The first success factor of Arhaus is its business model based on "made-in-America", thanks to its distribution centers spread all over the territory. This factor is a significant competitive advantage in the face of supply chain challenges. While its competitors are struggling with logistics, Arhaus can sell and deliver its products more quickly and at a lower cost. In addition, because of its focus on the high-end segment, Arhaus has more room for price growth.

The second success factor is online shopping. Beyond the obvious aspect that any retail company today must be exposed to online commerce to evolve, Arhaus has a very good growth rate on this specificity. Online sales represented nearly 20% - pandemic effect - of the turnover this year against only a few percent a few years ago. The group is increasingly focusing on its retail branch (which represents more than 80% of the turnover) which can rely on a network of 81 stores in more than 29 states.

The company's brand image is the third factor in this success. The group has relied in particular on social networks to make itself known and attract more of the public. The luxury brand has more than 1.2 million followers on Instagram. The quality of the stores and the website has also greatly helped the company to become a reference player in the home luxury market on the North American continent.

Source: Arhaus

Growth stock:

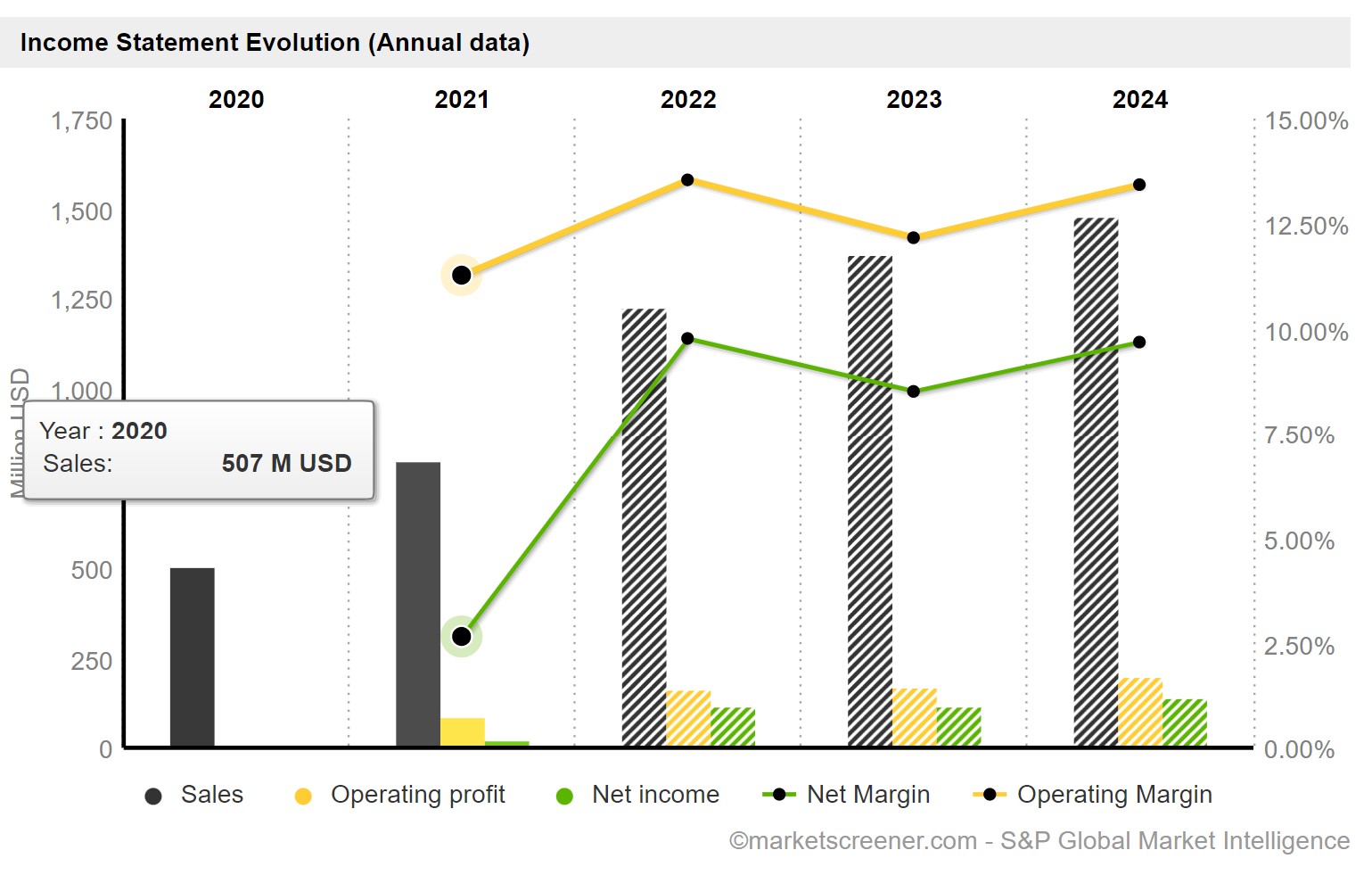

Revenues have doubled over the past few years, from $507 million to more than $1.2 billion in 2022, and are projected to reach $1.5 billion in revenues by 2024. Operating income has doubled over the same period (from $90 million to over $160 million), thanks to excellent cost control and R&D budgets.

Arhaus continues to invest heavily in its R&D activities to innovate and offer even more sustainable and environmentally friendly products. The company's net income is up by more than 400% over 1 year, from $21.1M to $120M for a net margin of nearly 9%. Arhaus's results are better than those of its competitors, which are around 5% margins, which is explained by an advantageous pricing-power for the group.

Arhaus has also grown through a series of acquisitions, starting in late 2010 with the purchase of Caluco allowing the company to expand into the market for garden furniture. Following this acquisition, It opened the Arhaus Studio division, which focuses on custom furniture design for professional and residential customers. Another significant acquisition was Lee Industries, in 2020, allowing Arhaus to further diversify its product line. The company has not yet tackled the international market, which could become the future growth driver and will undoubtedly prove to be crucial in the coming months and years.

Valuation:

The company is valued at 17 times 2022 earnings, well below its historical valuation at 73 times earnings, and in line with the sector at 20 times when the fundamentals here are much better. However, the market anticipates some slowdown in the sector's growth in these more complicated macroeconomic conditions. This slowdown should only be technical and would affect Arhaus less than its more dependent competitors.

The DCF model is built on several assumptions. Year-end sales are expected to be $1,227 million in the middle of the forecast range with 81 stores open, implying $15.1 million per store. Although the last 12-month gross margin is 44.9% which is quite conservative given the development of e-commerce and the opening of a new distribution center. Management expects adjusted EBITDA for the year to be $173-180 million, which projects approximately 8.5% of the operating margin for the year. The operating margin should increase by one percentage point in 2023 and remain at this level until the end of the forecast period. Management forecasts capital expenditures in the range of $55-65 million for the year, which corresponds to 5.5% of revenue at the upper end of the range.

All these arguments in favor of Arhaus lead me to believe that it is a little gem. I wouldn't be surprised to see the stock outperform almost all of its competitors in the coming months given its growth potential, operating track record and attractive valuation, all of which are better than the industry average. The company appears to be trading at a discount to its fair value. However, it is important for the group to further develop its e-commerce branch to gain share and thus avoid behemoths like Amazon from nibbling away at this market share.

Source: MarketScreener